For the reason that introduction of the web roughly three many years in the past, buyers have just about all the time had a buzzy pattern or innovation to captivate their consideration. Nonetheless, none of those different next-big-thing tendencies got here anyplace near rivaling what the web did for company America.

However after a protracted wait, the synthetic intelligence (AI) revolution has left skilled and on a regular basis buyers wide-eyed with its potential.

Though estimates range, as you’d anticipate from a game-changing expertise, the analysts at PwC see AI including $15.7 trillion (sure, with a “t”) to the worldwide financial system through numerous consumption-side advantages and productiveness beneficial properties by the flip of the last decade.

No firm has benefited extra instantly from the hype surrounding AI and its seemingly limitless ceiling than Nvidia (NASDAQ: NVDA).

Nvidia’s ascension is in contrast to something we have ever witnessed

When the web page turned to 2023, Nvidia was a $360 billion firm that was on the perimeter of being one among America’s most-important tech shares. However as of the closing bell on Aug. 28, 2024, it was price $3.09 trillion. In June, it briefly turned probably the most precious publicly traded firm, shortly after finishing its historic 10-for-1 inventory break up.

No deep digging is required to flesh out why Nvidia added, at one level, properly over $3 trillion in market worth in lower than 18 months. In brief order, the corporate’s H100 graphics processing unit (GPU) turned the popular chip in AI-accelerated knowledge facilities. It is successfully the mind that powers generative AI options, facilitates the coaching of enormous language fashions (LLMs), and fuels split-second decision-making by AI-driven software program and programs.

Demand for Nvidia’s {hardware} has fully overwhelmed provide. Producing the must-have AI-GPU has afforded Nvidia a jaw-dropping quantity of pricing energy. Whereas Superior Micro Units (NASDAQ: AMD) is promoting its MI300X AI-GPU for between $10,000 and $15,000, Nvidia’s H100 typically prices between $30,000 and $40,000.

Nvidia’s CUDA software program platform has performed a key position in its success, too. CUDA is the toolkit builders use to construct LLMs in addition to get as a lot computing capability out of their GPUs as attainable. CUDA has been an indispensable software that is helped preserve Nvidia’s prospects loyal to its ecosystem of services and products.

The tip results of this seemingly textbook growth has been six consecutive quarters the place the corporate’s reported gross sales and income fully trounced the consensus of Wall Avenue analysts.

However regardless of this success, one under-the-radar efficiency metric seems to all however affirm that Nvidia’s finest days are within the rearview mirror.

Story continues

The primary sequential decline in two years for this working metric spells bother

As I acknowledged earlier this week, I wasn’t going to be shocked one bit if Nvidia blew previous Wall Avenue’s consensus income and earnings per share (EPS) estimates for the fiscal second quarter (ended July 28) — which is exactly what it did. It isn’t unusual for analysts to be conservative with their estimates and supply a low sufficient bar for firms to clear.

However headline figures, corresponding to income and web earnings, solely seize a part of the story.

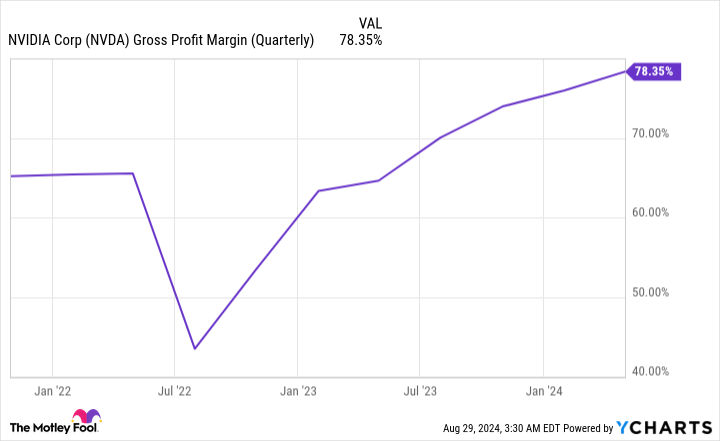

With Nvidia, the one efficiency metric that tells a extra thorough story about the place it is headed is its gross margin. Personally, I choose to make use of adjusted gross margin, which removes acquisition-related bills and stock-based compensation; however both gross margin or adjusted gross margin works nice for this dialogue.

Through the fiscal first quarter (ended April 28), Nvidia’s adjusted gross margin expanded to an virtually unthinkable 78.35%. In a span of 5 quarters, it is risen by near 14 proportion factors, which is a mirrored image of the corporate commanding such excessive value factors for its AI-GPUs.

Nonetheless, Nvidia additionally guided to an adjusted gross margin of 75.5% (+/- 50 foundation factors) for the fiscal second quarter in its first-quarter report. If it had been to hit this vary, it might mark the primary sequential quarterly decline in adjusted gross margin in two years.

After the closing bell on Wednesday, Aug. 28, Nvidia delivered its much-anticipated fiscal second-quarter working outcomes, with adjusted gross margin falling by 320 foundation factors to 75.15%. Whereas that is inside vary of what the corporate forecast three months prior, it is on the decrease finish of what was anticipated.

What’s extra, Nvidia’s fiscal third-quarter outlook requires the potential of further gross margin contraction, with an adjusted gross margin forecast of 75% (+/- 50 foundation factors).

Though its adjusted gross margin continues to be up considerably from the place issues stood 18 months in the past, there seems to be no query that the tide is popping — and never for the higher.

Aggressive pressures and historical past are working in opposition to Nvidia

Regardless that Nvidia is promoting extra of its H100 chips, and CEO Jensen Huang has famous that demand stays sturdy for its next-generation Blackwell GPU structure, the lion’s share of its adjusted gross margin growth has been the results of AI-GPU shortage and its otherworldly pricing energy.

The primary downside is that AI-GPU shortage will likely be abating over time. AMD has been rising manufacturing of its MI300X, and it would not have the identical provide constraints that Nvidia has contended with from main chip fabricator Taiwan Semiconductor Manufacturing (NYSE: TSM). As exterior rivals enter the house and ramp their output, Nvidia’s pricing energy will likely be steadily whittled away.

It is also extremely probably that suppliers are going to desire a larger piece of the pie. Taiwan Semiconductor is within the technique of meaningfully increasing its chip-on-wafer-on-substrate (CoWoS) capability, which is a necessity for packaging the high-bandwidth reminiscence wanted in AI-accelerated knowledge facilities. Rising its CoWoS capability is more likely to translate into increased prices on Nvidia’s finish to spice up manufacturing.

And it isn’t simply exterior competitors that this main AI juggernaut wants to fret about. Nvidia’s 4 largest prospects by web gross sales (all members of the “Magnificent Seven”) are growing in-house AI-GPUs to be used of their high-compute knowledge facilities. The H100 and Blackwell GPUs sustaining their computing capability benefits will not to be sufficient to dissuade these prime prospects from utilizing their in-house chips and denying Nvidia precious knowledge middle “actual property.”

The opposite main concern working in opposition to Nvidia is historical past. At no level during the last 30 years has there been a next-big-thing expertise, innovation, or pattern that is averted an early-innings bubble. All applied sciences want time to mature, and synthetic intelligence would not look like the exception to this unwritten rule.

Though Nvidia has loved massive orders from its prime prospects, the overwhelming majority of companies investing in AI lack a transparent sport plan. Even Meta Platforms, which is one among Nvidia’s prime 4 prospects by web gross sales, has no intention of meaningfully monetizing its AI investments anytime quickly.

This clear lack of path, coupled with the corporate’s adjusted gross margin forecast, successfully confirms that Nvidia’s inventory has peaked.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 finest shares for buyers to purchase now… and Nvidia wasn’t one among them. The ten shares that made the lower might produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $769,685!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of August 26, 2024

Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Sean Williams has positions in Meta Platforms. The Motley Idiot has positions in and recommends Superior Micro Units, Meta Platforms, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot has a disclosure coverage.

Nvidia’s Inventory Has Peaked, and 1 Underneath-the-Radar Efficiency Metric Proves It was initially printed by The Motley Idiot